Last Updated on 21 March 2022

The new tax year 2022/23 is just around the corner, and we are pleased to present our review of the main upcoming legislative changes which affect payroll.

There are some areas that see little or no change:

- The personal allowance remains at £12,570. Income tax rates and thresholds remain unchanged in England and Wales. In Scotland there is a small uplift in the starter and basic rate bands.

- Also unchanged is the Employment Allowance, remaining at £4,000 per annum, and the Apprenticeship Levy rate, allowance and pay bill threshold remain unchanged too.

- We see a small increase across the main Statutory Payments in 2022/23.

- Student Loan Plan 1 & Plan 4 thresholds see a small increase, the rate of deduction remains unchanged.

However, there are some significant changes:

- National Insurance has been temporarily increased. Employees’ contributions go from 12% to 13.25% (also 2% to 3.25%) and Employers from 13.8% to 15.05%

- This increase is to help support the NHS, but in 2023-24 the increase will be removed from National Insurance and become a separate deduction item, known as the Social Care Levy.

- The creation of Freeports and Greenports (in Scotland) will bring Employers National Insurance savings for qualifying employers.

- Employers of veterans can now enjoy 0% Employers National Insurance, assuming the qualifying conditions are met.

- The National Living Wage increases apply from 1st April the adult rate to £9.50 per hour, with the rate for 21-22 year olds increasing to £9.18.

More details on all these items are shown below.

In addition to all of this, we have provided a section called Other Topics with some extra information which you may find useful whether you are a payroll bureau client, or if you run your own payroll.

We would draw particular attention to the section on Salary Exchange as the impending National Insurance hike has made this a more attractive option for many employers. One of our colleagues, Ricky Clark, from Henderson Loggie Financial Planning recently produced a video on this topic which you can view below.

Income Tax

Income tax allowances set by the UK government for England, Wales Northern Ireland, and Scotland (not devolved). There will be no change to the personal allowances in 2022-23.

Income tax rates for England and Northern Ireland 2022-23. Income tax rates and thresholds are unchanged.

Income tax rates for Wales 2022-23. Income tax rates and thresholds are currently reflecting those set for England and Northern Ireland.

Income tax rates for Scotland 2022-23. There are some changes to the thresholds for the Starter and Basic rate bands.

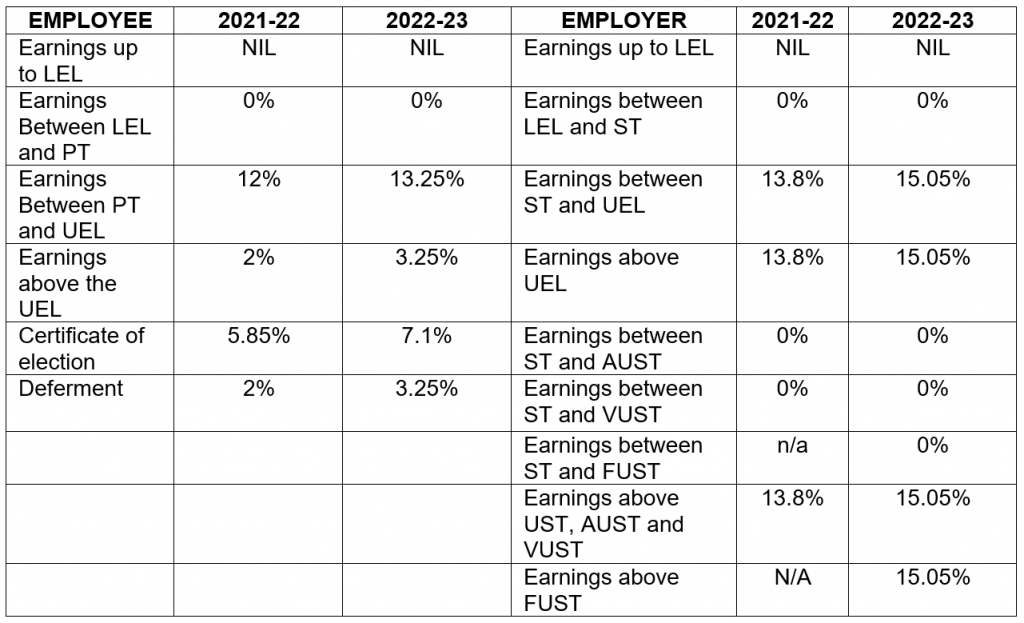

National Insurance and the Social Care Levy

From 6th April 2022 there will be a temporary increase in National Insurance Contribution rates payable on all earnings above the Primary Threshold. This is the first major change to National Insurance for several years. The purpose of this increase is to help support the NHS, but in 2023-24 this increase will no longer be part of National Insurance Contributions, it will change to a separate item known as Social Care Levy.

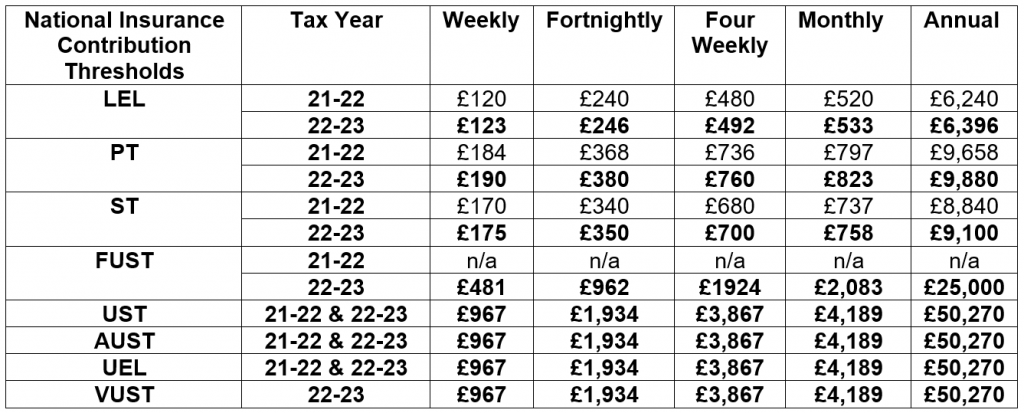

There is a small increase in the thresholds for National Insurance.

National Insurance Contribution Rates

Showing comparison between 2021-2022 and 2022-23 rates. (Applicable to the whole of UK)

National Insurance Thresholds

Explanation of terms

LEL – Lower Earnings Limit. Employees do not pay National Insurance when earning below this point.

PT – Primary Threshold. Employees start paying National Insurance once they reach this threshold.

ST – Secondary Threshold. Employers start paying National Insurance at this point.

FUST – Freeport Upper Secondary Threshold. Employers of freeport employees start paying National Insurance at this point

UST – Upper Secondary Threshold. Employers of employees who are under 21 pay zero rate up to this point.

AUST – Apprentice Upper Secondary Threshold. Employers of certain apprentices who are under 25

pay zero rate up to this point

UEL – Upper Earnings Limit. All employees pay a lower rate of National Insurance above this point.

VUST – Veterans Upper Secondary Threshold. Employers of employees who are veterans pay zero rate up to this point.

Freeports (known as Greenports in Scotland)

It was confirmed in the 2021 Budget that eight new Freeports would be created in England. Similar freeports could be opened in Wales, Scotland and Northern Ireland.

Employers operating within Freeport tax sites will be able to pay 0% employer class 1 NICs on the salaries of new employees working within Freeport tax sites up to the Freeport Upper Secondary threshold (FUST).

Veterans

This relief provides a zero-rate of secondary Class 1 National Insurance contributions (NICs) on the earnings of a qualifying veteran for 12 consecutive months from the first day of their first civilian employment after leaving the regular armed forces. This zero-rate can be applied up to the (new) Veteran’s Upper Secondary Threshold (VUST).

This relief is available from April 2021 so that employers can qualify for the relief as early as possible. From April 2021 to March 2022, employers will need to pay the associated Secondary Class 1 NICs as normal and then claim it back retrospectively from April 2022 onwards.

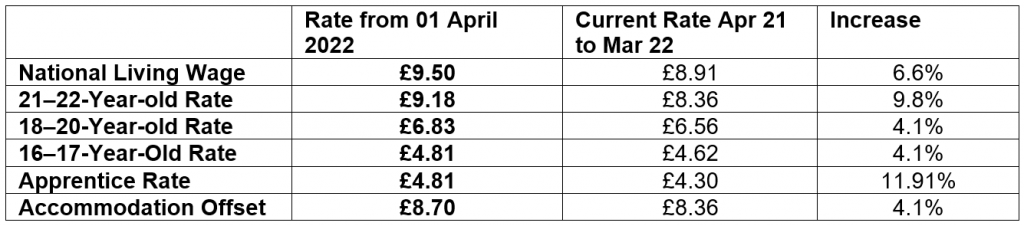

National Minimum Wage

The National Living Wage (NLW) will rise to £9.50 from 1 April 2022. This represents an increase of 59 pence or 6.6 per cent.

All increases to NMW apply from the employee’s next pay reference period.

- If you pay your employee on 29th April 2022 for the 1st to 30th April, then the increase applies on 1st April.

- If you pay your employee on 13th May 2022 for 16th April to 15th May, then the increase applies on 16th April.

- Many employers choose to increase from 1st April in the interest of fairness.

NMW is easy to calculate for hourly paid employees, but careful consideration needs to be given to those receiving an annual salary, paid per task etc. Consideration must also be given to employer deductions, and what constitutes working time, to name just a few.

It is very easy to get this wrong, so it is essential to ensure that a thorough checking system is in place to avoid falling foul of this legislation.

Student Loan

The student and postgraduate loans thresholds and rates are as follows:

Deductions for:

- Plans 1, 2 and 4 remain at 9% for any earnings above the respective thresholds.

- Postgraduate loans remain at 6% for any earnings above the respective thresholds.

Statutory Payments

Here are the rates and employer recovery information for the main statutory payments.

Statutory Sick Pay

The weekly rate of Statutory Sick Pay for the 2022-23 tax year is £99.35.

The same weekly Statutory Sick Pay rate applies to all employees. However, the amount you must pay an employee for each day they’re off work due to illness (the daily rate) depends on the number of ‘qualifying days’ they work each week.

Recovery – This is a cost borne by the employer, it is not recoverable from HMRC.

Statutory Paternity Pay

The weekly rate of Statutory Paternity Pay for the 2022-23 tax year is £156.66 or 90% of pay, whichever is lower.

Recovery – 92% is recoverable if the employee and employer total Class 1 National Insurance is above £45,000 for the previous tax year. 103% if your total Class 1 National Insurance for the previous tax year is £45,000 or lower.

Statutory Maternity Pay

90% of the employees’ average weekly earnings for the first 6 weeks, then £156.66 or 90% of pay, whichever is lower for the remaining weeks (up to a further 33 weeks).

Recovery – 92% is recoverable if the employee and employer total Class 1 National Insurance is above £45,000 for the previous tax year. 103% if your total Class 1 National Insurance for the previous tax year is £45,000 or lower.

Employment Allowance

There are no changes to Employment Allowance for the 2022-23 tax year. You can claim Employment Allowance if you are a business or charity and your employers’ Class 1 NIC total in the preceding tax year was less than £100,000. Remember that Class 1 NIC on payments to off-payroll workers do not count towards this threshold.

There are some exemptions to eligibility for employment allowance. If your business is part of a group, if you have more than one payroll, if de minimis state aid rules apply to you, your eligibility will be affected.

Apprenticeship Levy

The Apprenticeship Levy is a charge that applies to all UK employers who have a pay bill exceeding £3 million. A pay bill is based on the total amount of earnings which an employer is liable to pay Class 1 secondary NICs on.

The Apprenticeship Levy is charged at a rate of 0.5% on an employer’s annual pay bill. Employers are given an annual Apprenticeship Allowance of £15,000. This means that only those employers with an annual pay bill of over £3 million will have to pay, and report, the levy because 0.5% of an employer’s £3 million pay bill is £15,000, which is fully removed by the Apprenticeship Levy allowance.

Other Topics

Childcare Vouchers

The Government closed the Childcare Vouchers scheme to new entrants on 4th October 2018.

Employees currently in the scheme can still exchange salary for child care vouchers subject to the following limits:

A basic earnings assessment must be carried out for all childcare voucher recipients to ensure that the correct exemption limits are being applied.

Employees looking to join Childcare Vouchers for the first time must be told the option is no longer available to them. The Government launched a new scheme called Tax-Free Childcare. Employees must apply for this directly online with HMRC.

Salary Exchange

A salary exchange scheme (also known as a salary sacrifice scheme) can create significant savings for employers, this has come more into focus with the temporary increase in National Insurance Contributions.

A salary exchange arrangement is an agreement to reduce an employee’s entitlement to cash pay, usually in return for a non-cash benefit.

As an employer, you can set up a salary exchange arrangement by changing the terms of your employee’s employment contract. Your employee needs to agree to this change.

A salary exchange arrangement must not reduce an employee’s cash earnings below the National Minimum Wage (NMW) rates. Employers must put procedures in place to cap salary exchange deduction and ensure NMW rates are maintained.

Schemes that do not have to report to HMRC for a salary exchange arrangement are:

- payments into pension schemes

- employer provided pensions advice

- workplace nurseries

- childcare vouchers and directly contracted employer provided childcare that started on or before 4 October 2018

- bicycles and cycling safety equipment (including cycle to work)

Where an employee gives up a portion of their salary in exchange for one of these benefits, the employee and employer will make savings, because they do not pay tax or national insurance on the sacrificed amount.

Workplace pensions

There is no change to the auto enrolment earnings trigger, this remains at £10,000 per annum.

In addition to this, the government confirmed that the qualifying earnings band (the band of earnings that minimum AE contributions are based on) has been frozen for the first time for 2022/23, meaning that earnings between £6,240 and £50,270 will qualify.

Contribution rates for employers and employees, where the minimum for a qualifying pension scheme in 2022/23 remains at 8% total contributions (including tax relief) on relevant earnings, of which at least 3% is from the employer.

Public Holiday in June

In November 2020, the Government announced an extra bank holiday for June 2022. The late May Bank Holiday has been moved to Thursday, 2 June 2022 with the additional Platinum Jubilee bank holiday falling on Friday, 3 June 2022. This creates a four-day weekend for some.

Employers will need to consider how this extra bank holiday impacts their workforce availability.

Are your employees entitled to this extra bank holiday? This very much depends on the wording in their Contract of Employment, demonstrated by this example:

- If the contract of employment states X days’ holiday, plus public and/or bank holidays

- There will be entitlement to this extra bank holiday as the contract does not state the exact number of bank holidays the employee is entitled to, and clearly states that bank holidays are on top of annual holiday allowance.

- If the contract of employment states X days’ holiday, inclusive of all public and/or bank holidays

- There is no contractual right to this extra day, as public and/or bank holidays are included in a set number of holiday days entitlement, although the employer may choose to grant it in any case.

The wording of your contracts of employment are key here, it would be advisable to review this with your HR or employment law adviser and let your employees know their position.

More Information

You can read HMRC’s full guidance on the rates and thresholds for employers 2022/23 here.