As someone who spends a lot of time thinking about how numbers tell a story, I’ve been reflecting on the upcoming changes to FRS 102 – and what they mean for businesses.

If you’re a mid-sized, privately owned business – especially in a service sector with long-term contracts or significant lease commitments – the upcoming changes to FRS 102 are likely to reshape how your performance is reported, and this article is written with you in mind.

These changes, effective January 2026, bring UK Generally Accepted Accounting Practice (GAAP) closer to International Financial Reporting Standards (IFRS), with updates to revenue recognition1 and lease accounting2.

But beyond compliance, these changes could significantly affect how your performance is reported – and how your business is valued.

Revenue Recognition: Timing is Everything

The new five-step model for revenue recognition means income will only be recognised when promises in a contract are fulfilled – not just when cash is received or invoices are raised.

For businesses with multi-year contracts, this could mean revenue is recognised later than before. That in turn affects Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA), short-term profitability, and potentially, how attractive a business looks to investors or lenders.

Lease Accounting: Debt in Disguise

Under the revised FRS 102, most leases must now appear on the balance sheet if you’re a lessee. Lease expenses will now appear as depreciation and interest – boosting EBITDA but increasing reported debt.

Right-of-use assets are recognised for lease contracts, and a corresponding liability being the payments to be made under the lease.

This change doesn’t just affect optics, it alters key metrics like net assets, gearing, and interest cover.

Valuation Implications: Beyond the P&L

These accounting changes don’t change the underlying economics – but they do change how those economics are presented. And that matters.

Valuations based on earnings or net assets could vary significantly depending on contract timing and accounting treatment. Without deeper analysis, businesses risk being over- or undervalued as illustrated in the examples below.

Example 1:

A software company was recognising a £100,000 3-year contract, including a license fee (£50k) and support (£50k), over the 3 years. Under the new rules, the license fee is recognised upfront, while support is spread over time. The result? EBITDA spikes in year one, dips in years two and three – and valuations based on earnings could swing dramatically depending on timing:

Table 1: Revenue Recognition and EBITDA

If valuation was carried out in year 1, and the underlying contract terms were ignored, the valuation post-FRS 102 changes would be significantly higher.

Results will vary by contract, as the impact depends on contract structure and performance obligations.

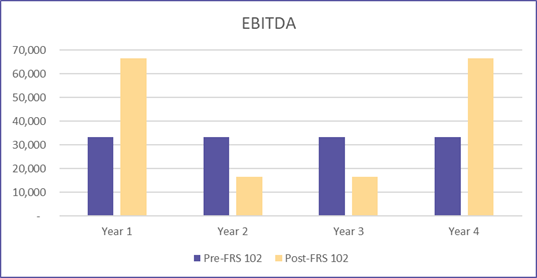

Example 2:

Say this same software company signed a five-year lease on 1 January 2024 to lease an office building. Lease rentals are £25,000 per annum, payable monthly.

In the 2 years to 31 December 2025, the company recognised £25,000 per annum as an expense in their profit and loss statement as it was recognised as an operating lease under previous FRS 102 criteria.

Accounting for this following the changes to FRS 102 would result in EBITDA improving by £25k each year. Although the lease expense is replaced by depreciation and interest, these sit below EBITDA.

Assuming depreciation over 4 years and an effective interest rate of 7% this would result in the following:

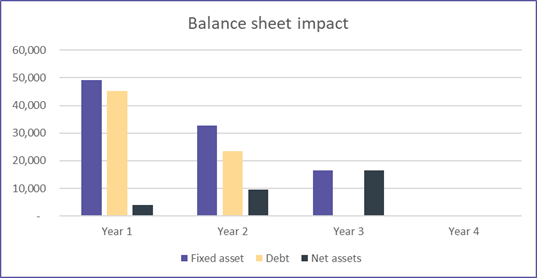

Table 2: Lease Accounting and Financial Position

It’s not just optics that are affected. The changes to lease accounting impact key metrics including net assets, gearing, and interest cover.

Net assets overall would improve over the first three years in the above example; however, debt would also increase compared to pre-FRS 102 changes. This would impact any net asset valuation, and an earnings-based valuation would increase as expenses are removed, and the resulting depreciation and interest are not included within EBITDA. Additionally, net cash or debt would need adjusted and would impact the equity value.

NB: the outcome of this will depend on lease amortisation schedules and interest rates. Therefore, net assets may improve depending on the lease terms.

Therefore, from a valuation perspective, deeper analysis is required. Understanding the timing and substance behind reported figures is essential, not just what appears on the profit and loss statement.

Other considerations:

Changes to FRS 102 introduce updated principles for fair value measurement. This may impact how businesses measure certain assets and liabilities, potentially impacting the value of net assets.

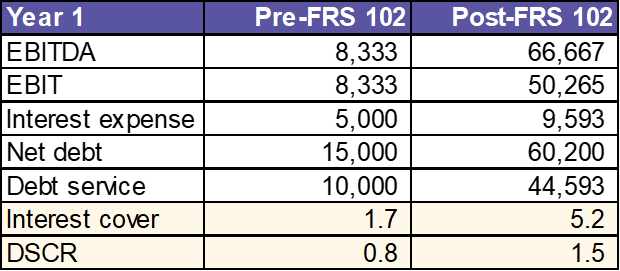

Covenants and Ratios: Time for a Rethink?

As shown in example 2 above, the changes to FRS 102 can impact both EBITDA, increase interest expenses and increase debt on the balance sheet.

This in turn can have a significant impact on any covenants being monitored and how debt is structured. Using the above examples to illustrate:

Other ratios impacted include gearing, return on assets, working capital ratio and net profit margin.

Debt service coverage, interest cover, and gearing ratios may all shift – even if cash flow doesn’t. That could trigger covenant breaches or require renegotiation, particularly for businesses with tight margins or complex financing.

Early engagement with lenders is key. So is educating your stakeholders, as these changes could affect KPIs, bonuses and dividend capacity.

What Should You Do Next?

Valuations could vary significantly depending on contract timing and accounting treatment. So what should you do next?

- Model the impact: Work with your accountant to understand how these changes affect your numbers.

- Engage stakeholders early: Lenders, investors, and board need to understand the story behind the numbers. Communicating proactively can help prevent covenant breaches.

- Educate your teams: Financial KPIs may need to be redefined.

- Look beyond compliance: These changes are an opportunity to rethink how you measure and communicate value.

If these changes apply to your business, now is the time to dig deeper — not just into the numbers, but into the story they tell. Understanding how FRS 102 reshapes your financial narrative could be the difference between missed opportunities and strategic advantage.

If you want to find out how it might impact the value of your company, please reach out to our corporate finance team.

[1] ACCA Technical Factsheet – Revenue recognition under FRS 102 (September 2024)

[2] ACCA Technical Factsheet – Lease accounting under FRS 102 (October 2024)

Get in touch

Last Updated on 7 November 2025