The new tax year 2023/24 is just around the corner, and we are pleased to present our review of the main upcoming legislative changes which affect payroll.

There are some areas that see little or no change, and some changes are more significant:

- The personal allowance remains at £12,570.

- The threshold for the additional rate of income tax is lowered in Scotland, Wales, and England & Northern Ireland.

- In Scotland, the higher rates of taxation increase by 1%.

- National Insurance rates and thresholds stay at the amounts in place since November 2022. Note for the 2022-23 year, due to the changes in rates that took place in July and November, directors will see a blended rate of national insurance applied when the annual recalculation is performed. The rates are 14.53% employer and 12.73% & 2.73% employee.

- Also unchanged is the Employment Allowance, remaining at £5,000 per annum, and the Apprenticeship Levy rate, allowance and pay bill threshold remain unchanged too.

- We see a small increase across the main Statutory Payments in 2023/24.

- Student Loan Plan 1 & Plan 4 thresholds see a small increase, the rate of deduction remains unchanged.

- The National Living Wage increases are significant this year and they apply from 1st April. The adult rate increases to £10.42 per hour, with the rate for 21-22 year olds increasing to £10.18.

More details on all these items are shown below along with a link to HMRC’s full guidance.

In addition to all of this, we have provided a section called Other Topics, some extra information which you may find useful whether you are a payroll bureau client, or if you run your own payroll.

We recently provided a guide to some of the things we recommend you review ahead of payroll year end, some of which are time sensitive. Here is the link in case you missed this: Are you ready for payroll year-end? A helpful checklist

If you have any questions about any of the upcoming legislative changes which affect payroll and would like to get in touch with our team, please contact us at payroll2@hlca.co.uk or call 01382 200055.

Income Tax

Income tax allowances set by the UK government for England, Wales Northern Ireland, and Scotland (non-devolved) There will be no change to the personal allowances in 2023-24

Income tax rates for England and Northern Ireland 2023-24. The threshold the for additional rate of income tax is lowered

Income tax rates for Wales 2023-24. Income tax rates and thresholds are currently reflecting those set for England and Northern Ireland.

Income tax rates for Scotland 2023-24. There are two key changes – an increase in the higher rates of taxation by 1% and the alignment of the highest threshold to the UK gov additional rate limit.

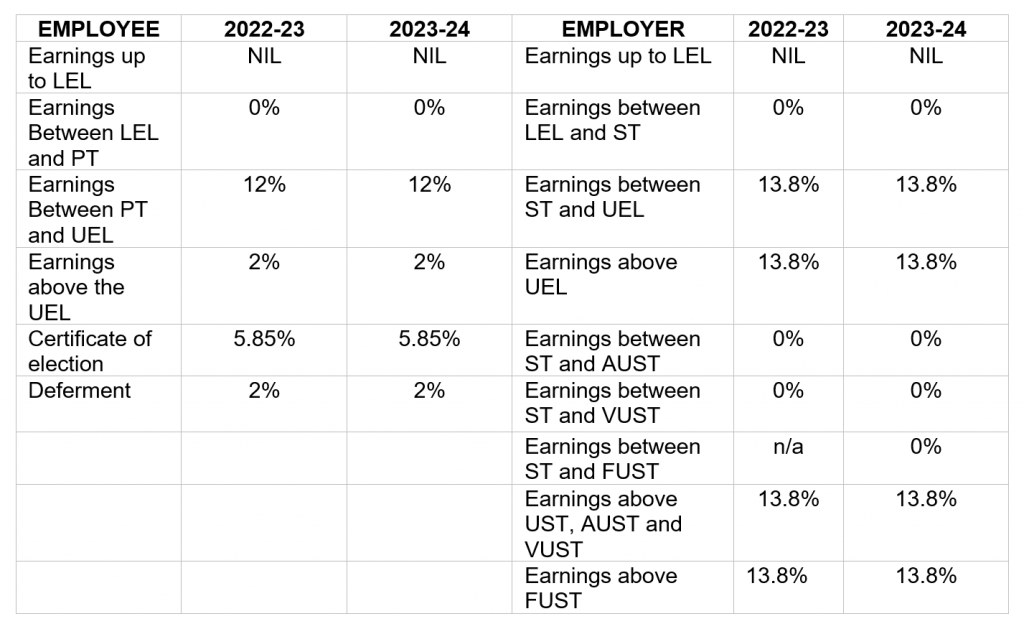

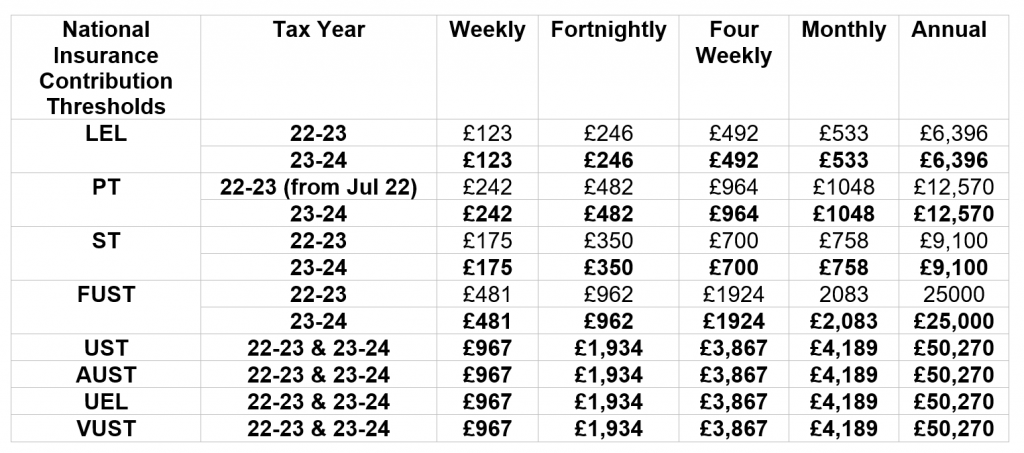

National Insurance

National Insurance Contribution Rates

NIC rates were raised in April 2022 and then lowered back to the original rates in November 2022. The rates for 2023/24 remain at the amounts set in November 2022. (Applicable to the whole of the UK)

National Insurance Thresholds

Explanation of terms

LEL – lower earnings limit. Employees do not pay National Insurance when earning below this point.

PT – primary threshold. Employees start paying National Insurance once they reach this threshold.

ST – secondary threshold. Employers start paying National Insurance at this point.

FUST – freeport upper secondary threshold. Employers of freeport employees start paying National Insurance at this point.

UST – upper secondary threshold. Employers of employees who are under 21 pay zero-rate up to this point.

AUST – apprentice upper secondary threshold. Employers of certain apprentices who are under 25

pay zero-rate up to this point

UEL- upper earnings limit. All employees pay a lower rate of National Insurance above this point.

VUST – veterans upper secondary threshold. Employers of employees who are veterans pay zero-rate up to this point.

Freeports (known as Greenports or Green Freeports in Scotland)

What are freeports?

Freeports aim to create economic activity – like trade, investment, and jobs – near shipping ports or airports.

There are several freeports now in operation in England, and plans for Scotland and Wales are currently in development.

Employers operating within Freeport tax sites will be able to pay 0% employer class 1 NICs on the salaries of new employees working within Freeport tax sites up to the Freeport Upper Secondary threshold (FUST).

Veterans

This relief provides a zero-rate of secondary Class 1 National Insurance contributions (NICs) on the earnings of a qualifying veteran for 12 consecutive months from the first day of their first civilian employment after leaving the regular armed forces. This zero-rate can be applied up to the (new) Veteran’s Upper Secondary Threshold (VUST).

This relief is available from April 2021 so that employers can qualify for the relief as early as possible. From April 2021 to March 2022, employers will need to pay the associated Secondary Class 1 NICs as normal and then claim it back retrospectively from April 2022 onwards.

National Minimum Wage

The National Living Wage (NLW) will rise to £10.42 from 1 April 2023. This represents an increase of 92 pence or 9.7 per cent.

All increases to NMW apply from the employee’s next pay reference period.

- If you pay your employee on 28th April 2023 for the 1st to 30th April, then the increase applies on 1st April.

- If you pay your employee on 12th May 2023 for 16th April to 15th May, then the increase applies on 16th April.

- Many employers choose to increase from 1st April in the interest of fairness.

NMW is easy to calculate for hourly paid employees, but careful consideration needs to be given to those receiving an annual salary, paid per task etc. Also, consideration must be given to all elements which are factored into NMW compliance, such as employer deductions, and what constitutes working time, to name just a few.

It is very easy to get this wrong, so it is essential to ensure that a thorough checking system is in place to avoid falling foul of this legislation.

Student Loan

The student and postgraduate loans thresholds and rates are as follows:

Deductions for:

- Plans 1, 2 and 4 remain at 9% for any earnings above the respective thresholds.

- Postgraduate loans remain at 6% for any earnings above the respective thresholds.

Statutory Payments

Here are the 2023/24 rates and employer recovery information for the main statutory payments.

Statutory Sick Pay

The weekly rate of Statutory Sick Pay for the 2023-24 tax year is £109.40.

The same weekly Statutory Sick Pay rate applies to all employees. However, the amount you must pay an employee for each day they’re off work due to illness (the daily rate) depends on the number of ‘qualifying days’ they work each week.

Recovery -This is a cost borne by the employer, it is not recoverable from HMRC.

Statutory Paternity Pay

The weekly rate of Statutory Paternity Pay for the 2023-24 tax year is £172.48 or 90 % of pay, whichever is lower.

Recovery – 92% is recoverable if the employee and employer’s total Class 1 National Insurance is above £45,000 for the previous tax year. 103% if your total Class 1 National Insurance for the previous tax year is £45,000 or lower

Statutory Maternity Pay

90% of the employee’s average weekly earnings for the first 6 weeks, then

£172.48 or 90% of pay, whichever is lower for the remaining weeks (up to a further 33 weeks)

Recovery – 92% is recoverable if the employee and employer’s total Class 1 National Insurance is above £45,000 for the previous tax year. 103% if your total Class 1 National Insurance for the previous tax year is £45,000 or lower.

Employment Allowance

Employment Allowance for the 2023-24 tax year is set at £5,000. You can claim Employment Allowance if you are a business or charity and your employers’ Class 1 NIC total in the preceding tax year was less than £100,000. Remember that class 1 NIC on payments to off-payroll workers do not count towards this threshold.

There are some exemptions to eligibility for employment allowance. If your business is part of a group, if you have more than one payroll, and if de minimis state aid rules apply to you, your eligibility will be affected.

Apprenticeship Levy

The Apprenticeship Levy is a charge that applies to all UK employers who have a pay bill exceeding £3 million. A pay bill is based on the total amount of earnings which an employer is liable to pay Class 1 secondary NICs on.

The Apprenticeship Levy is charged at a rate of 0.5% on an employer’s annual pay bill. Employers are given an annual Apprenticeship Allowance of £15,000. This means that only those employers with an annual pay bill of over £3 million will have to pay, and report, the levy because 0.5% of an employer’s £3 million pay bill is £15,000, which is fully removed by the Apprenticeship Levy allowance.

Other Topics

Childcare Vouchers

The Government closed the Childcare Vouchers scheme to new entrants on 4th October 2018.

Employees currently in the scheme can still exchange salary for childcare vouchers subject to the following limits:

A basic earnings assessment must be carried out for all childcare voucher recipients to ensure that the correct exemption limits are being applied.

Employees looking to join Childcare Vouchers for the first time must be told the option is no longer available to them. The Government launched a new scheme called Tax-Free Childcare. Employees must apply for this directly online with HMRC.

Salary Sacrifice

A salary sacrifice scheme can create significant National Insurance savings for employers.

A salary sacrifice arrangement is an agreement to reduce an employee’s entitlement to cash pay, usually in return for a non-cash benefit.

As an employer, you can set up a salary sacrifice arrangement by changing the terms of your employee’s employment contract. Your employee needs to agree to this change.

A salary sacrifice arrangement must not reduce an employee’s cash earnings below the National Minimum Wage (NMW) rates. Employers must put procedures in place to cap salary sacrifice deductions and ensure NMW rates are maintained.

Schemes that do not have to report to HMRC for a salary sacrifice arrangement are:

- payments into pension schemes

- employer-provided pensions advice

- workplace nurseries

- childcare vouchers and directly contracted employer-provided childcare that started on or before 4 October 2018

- bicycles and cycling safety equipment (including cycle to work)

Where an employee gives up a portion of their salary in exchange for one of these benefits, the employee and employer will make savings because they do not pay tax or national insurance on the sacrificed amount.

Workplace pensions

The DWP has announced the annual thresholds for the 2023/24 tax year are unchanged, so stay the same as the 2022/23 year.

Contribution rates for employers and employees, where the minimum for a qualifying pension scheme in 2023-24 remains at 8% total contributions (including tax relief) on relevant earnings, of which at least 3% is from the employer.

Public Holiday in May

This year, we’ll get an extra bank holiday for King Charles III’s coronation which takes place on Monday 8th May. This takes the 2023 bank holidays to nine in total.

Employers will need to consider how this extra bank holiday impacts their workforce availability.

Are your employees entitled to this extra bank holiday? This very much depends on the wording in their Contract of Employment, demonstrated by this example:

- If the contract of employment states X days’ holiday, plus public and/or bank holidays

- There will be an entitlement to this extra bank holiday as the contract does not state the exact number of bank holidays the employee is entitled to and clearly states that bank holidays are on top of the annual holiday allowance.

- If the contract of employment states X days’ holiday, inclusive of all public and/or bank holidays

- There is no contractual right to this extra day, as public and/or bank holidays are included in a set number of holiday days entitlement, although the employer may choose to grant it in any case.

The wording of your contracts of employment are key here, it would be advisable to review this with your HR or employment law adviser and let your employees know their position.

Annual Leave Entitlement

The contract of employment stipulates employees’ annual leave entitlement, but as a minimum, the entitlement is:

- 4 weeks of annual leave

- 1.6 weeks of public/bank holiday leave

This gives a total of 5.6 weeks, regardless of whether the employee is full or part-time

- For a full-time Monday to Friday worker, this translates to:

- 20 days annual leave and 8 days of public/bank holiday leave, totalling 28 days per annum.

- If the worker is part-time and works three days per week, then this entitlement will reduce pro-rata to:

- 12 days annual leave and 4.8 days of public/bank holiday leave, totalling 16.8 days per annum

When it comes to valuing the holiday, if an employee receives a fixed pay, then they will be entitled to (using the full-time example) 5.6 weeks x weekly pay.

However, If the employee works varying hours, or received bonuses, commission, overtime etc, their holiday pay should be based on an average amount paid over the last 52 weeks worked.

Where the employee works some weeks and not others, the unworked weeks are skipped for this calculation and the weeks are counted back to a maximum of 104 weeks.

This exercise can be time-consuming and impractical, so a good holiday tracking system is essential.

Important points to note:

Rolled-up holiday pay is not allowed – this is where the employer adds an amount onto the employee’s hourly rate to cover holiday pay. Holidays must be paid for when taken.

Paying out holidays – the only time it is possible to pay out an accrued amount of holiday pay is when an employee leaves. An employee can arrange to sell holidays in excess of the statutory amount, this is an arrangement made between the employee and employer. The overriding principle when it comes to holiday pay is, holiday pay is there to facilitate payment during breaks, it is not for financial gain.

12.07% calculation method is unlawful – however, BEISS are currently reviewing the 52-week calculation method, as it can produce some unfair results. We hope this will result in a system which is fairer and easier to manage.

HMRC

Here is a link to HMRC’s full guidance: Rates and thresholds for employers 2023 to 2024